cwah

Member of DD Central

Posts: 949

Likes: 468

|

Post by cwah on Jul 15, 2020 21:03:36 GMT

I've no experience at using IB but the message sounds like they allow only OTC trades (where a trader buys the bonds to other by phone, old style). Be careful, not every Börse Frankfurt bond can be bought on Degiro. The USD ones are almost never available. At same maturity I found the bonds always better than Mintos, except the Mogo where Mintos is still competitive since the short term bond is almost at par now. Meanwhile, my lovely Iute is still rising  what is Iute?

|

|

|

|

Post by jmn on Jul 16, 2020 20:50:23 GMT

www.boerse-frankfurt.de/bond/xs2033386603-iutecredit-finance-s-a-r-l-13-19-23As expected 4finance is going down since it's too late to claim the vote bonus. I cancelled my order on Mogo-21 and instead bought all Sebo loans on Mintos with lower maturity (max 7m) and >13 yield, both Pri and Sec market. A 5-digit investment...  Money took 5 days to get transfered due to AML checks. As P2PMillionaire I invest through a legal entity for tax efficiency, but accounting is a bit more complicated. Sebo is about to be merged with Mogo, so I saw it as a good deal.

|

|

|

|

Post by jmn on Jul 22, 2020 14:37:42 GMT

|

|

|

|

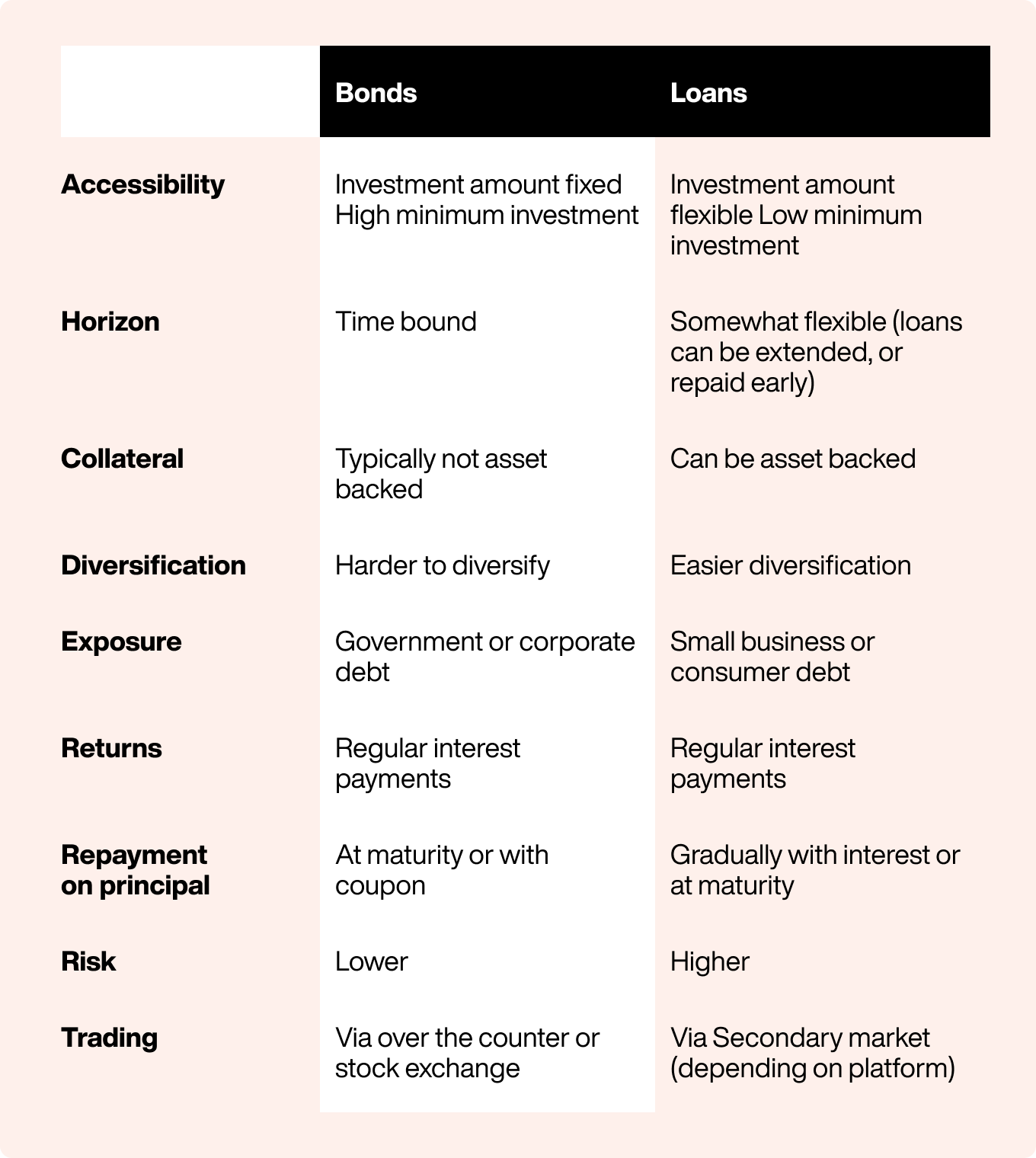

Post by geldregiertdiewelt on Jul 23, 2020 20:40:39 GMT

Mintos put this out today:  |

|

|

|

Post by jmn on Jul 23, 2020 23:16:10 GMT

Accessibility: Correct. Bond is multiples of 1000 (or 100'000 for institutional bonds), Mintos is Multiple of 0.01

However when you invest seriously, you do it in the 10K slices like P2PMillionaire. I'm tired of Fire blogs with portfolios in the hundreds who cry they lost 50€ in Kuetzal.

Horizon: Nope. All are both callable and extendable, like 4finance a couple days ago. And Bond extension requires agreement of bondholders. Bonds can be sold on sec market even during bankrupcy, like Wirecard. No 0.85% fee, no suspension like Mintos.

Collateral, Exposure: nope. Both are about lending money to companies. If a company bankrupts, no care the Mintos loans were backed or repaid. See Capital Service for example. Mintos loans are weak and unregulated, defaulting a Bond is another story.

Diversification : really? The bond market is 10 orders of magnitude larger than P2P. Even when restricted to the Junk sector. OK I admit P2P allows to go deeper in the Junkness by lending to exotic LO like Cashwagon or Getbucks. It's a point, not sure it's a good one. About duration, true Mintos range is larger, from 1 day to 20 years.

Returns: Correct, and it's even better on Mintos since period is one month, against one quarter at best for bonds.

Repayment: yes... It depends on the product, and it's quite an accounting detail, but yes Mintos loans are more often amortized.

Trading: if it's about selling, yes. P2P Platforms have either sec. Market, buyback like Moncera, or nothing like Lendermarket.

Risk: yes, but for various reasons:

1. The average Bond is non-junk, so, low risk.

2. Even if restricted to Junk, bonds tend to be senior, and are regulated.

3. Bonds have no platform risks.

4. But may a bond issuer LO bankrupts, Bond recovery won't probably be that better than Loan recovery.

5. LO can mock Mintos by just not sending money like Akulaku. You don't make fun of a regulated market.

Fees: I add this topic. P2P usually has no fees, so you can play with short-term, small sized loans. Bonds make you pay a non-negligible fee in all cases.

Tax: It depends a lot on your tax residency, but P2P is probably worse. In Belgium you pay no tax on discounts for example, but because Mintos accounts the discount as a Gain, so It becomes taxable.

Legal person: P2P platforms virtually all allow legal persons to invest easily, for free. Registering a legal person on a Broker site ranges from impossible to overpriced.

My opinion: yes P2P loans are assets, and are good for some cases:

* Short term treasury yielding

* SME legal persons

* Play money for small investments (low entry point, no need to amortize a fee)

* Far easier access of a LO loan than the respective bond, even with Degiro. Exemple: DelphinGroup.

|

|

|

|

Post by jmn on Jul 28, 2020 15:23:49 GMT

Mogo-21 is now at par!

All other tradable LO Bonds (non-Baltic) are skyrocketing, Mogo-22@86 4Finance-22@92.25 Iute-23@95 I wish I went into those assets before loosing €€€ into those Mintos things  I more or less compensated my Varks and Cashwagon losses with the LO bonds. My main portfolio being USD (like NomadCapitalist) i also lose as much on EUR/USD change that i won from coupons. 2020 had been a flat year for me so far.

|

|

|

|

Post by geldregiertdiewelt on Aug 1, 2020 19:56:37 GMT

|

|

|

|

Post by jmn on Aug 1, 2020 20:18:28 GMT

Hello,

Sure, all bonds i commented here are in the Junk category, hence while they bear 10+ yield.

My point was to compare them to Mintos. Like for Mogo or Iute where both are available. Basically, Bonds wins almost all points, and are getting better with prices raising back to par, while Mintos is getting worse with more ans more fees.

Is it better to buy 10000€ worth of Iute bond rather Iute loans on Mintos? Yes. Is it a good idea overall? Time will tell, but sure it's high risk compared to general Finance.

Again, this forum is about P2P so my comments make sense in a P2P-centric world.

|

|

|

|

Post by geldregiertdiewelt on Aug 17, 2020 18:10:09 GMT

....

DelfinGroup: Dedicated platform: no. Bonds: Yes (Baltic) My new favorite Mintos LO. I had tons of their sweet 13-16% loans they issued in the heart of Covid times that all got bought back. It sounds like Creditstar, but they did it the right way. This move is documented in their financial report, they never had any Pending Payment (except the legit ones like weekends/holydays) and they don't artificially extend forever their older low yield loans. So I'm happy in front of people who know how to deal with their money. Unable to invest into their bonds, I use their short-term Pawnbroker (well secured) 8% loans as an indirect Saving account for my treasury, since I don't see a possible loss with jewel-secured loans at a 30 day term. .... but I did not find a respective news on Delfin's own website www.delfingroup.lv/news

|

|

|

|

Post by jmn on Aug 18, 2020 7:25:16 GMT

Correct, their website hasn't been updated yet. It trades at ~101.5%, leading to a YTM of ~13.5% for 3 years, almost double of the Mintos yield of 8%. But in case of Mintos, it's fee-free and available for durations of 1 month or less. Good for treasury, but not as investments. For long term, any LO Bond is actually far better. Did any 4Finance bondholder actually receive the +0.5% vote bonus? It's overdue for weeks now and I still got nothing. Sounds like Mintos |

|

|

|

Post by happylemon on Aug 19, 2020 18:02:57 GMT

Did any 4Finance bondholder actually receive the +0.5% vote bonus? It's overdue for weeks now and I still got nothing. Sounds like Mintos Why you say overdue. Just go to their website and read the Announcement of Result: " The Terms and Conditions of the EUR bonds are expected to be formally amended in late August, once the statutory contestation period has expired. Subsequently, the amendment and participation fees will be paid to the relevant investors, and the Group’s operating entity in the Czech Republic will be added to the list of guarantors for its EUR and USD bonds. The full documentation is available on the Group’s website at www.4finance.com/investors-and-media/bonds/. " www.4finance.com/wp-content/uploads/2020/07/4finance-EUR-bondholders-approve-maturity-extension.pdf

|

|

|

|

Post by jmn on Aug 24, 2020 8:59:42 GMT

|

|

|

|

Post by jmn on Sept 1, 2020 13:50:02 GMT

Updates4FinanceThey published new results for H12020. I found them mild with less volume and high provisions, but it looks the market appreciated since the Bond value jumped to 96. I'm still waiting for my 0.75% Vote bonus...IuteCreditThe bonds stopped increasing and stabilized around 93. I continue to see them as a good deal, the discount is still high, the yield among the best and their financials solid. CreditStarPretty much the same as before, but amplified. My LenderMarket experience went better with everything bought back and paid on time, according to the new Terms (max 180 day extension), while on Mintos I still got zero buyback, with some loans going above the 180D limit. Mintos says it's legit when due to Covid. I'm getting tired of those improvised rules changes. Note on LenderMarket rates dropped to 12%, except for long term loans. If you have faith Creditstart will be alive in 1, 2 or 3 years, those loans are a good alternative to their similar yielding Bonds. RobocashAs expected, they are going toward quality with audited results up to 2019 (which is quite useless since Covid changed the game completely, but that's a nice idea) and they lowered their rates to 12% from 14%. I'm still dubious about why lending at 2.99% per day to give back investors 1.17% per month (before) and now 1.00% per month. Does it make such a big difference? MogoLike 4Finance their results are mild/weak but the bonds rise. I got some long Pending Payments for Latvia Car loans (and received zero PP compensation even for the 7D+ ones...) but the LV bond got still stronger. I don't sell but won't increase my position. USDI rant about Mintos and Creditstar, but my losses due to the collapse of USD are an order of magnitude larger. I'm wondering if I should enrage more to lose 5% on USD/EUR change or in the various Mintos LO failures. Edit: I finally received the 4Finance bonus. Edit: the discount is still highNo more. The Iutecredit bond jumped to 100 today. Wow

|

|

|

|

Post by jmn on Sept 15, 2020 17:38:37 GMT

Updates. Creditstar: The gap between Mintos and Lendermarket increases. The Mintos loans are really extended forever, like this one. It was already 180D+ extended and it got extended 60D more. Mintos blatantly never enforces any rule. I could complain to support but I won't. I'm just tired of that. On the other hand, Lendermarket maintained the 14% yield and now offers 2% cashback. So I'm moving the remnants of my Mintos portfolio to Lendermarket. The cashback will compensate for the Mintos fee. 4Finance, IuteCredit: the bonds still have a Bull trend, but with some volatility. Iute is no longer at 100 but this time it's 4Finance who almost reached that price. Mogo: same opinion as before. The 2021 expiry bond is too expensive, the USD one is not available and the 2022 looks too weak, I just don't buy. Robocash: Ditto. I keep a positive eye on them, but 12% no-bonus won't make me invest. Updates. (edit) Kristaps Mors dropped an interesting negative article about Creditstar. I note that while their short term (sic) pre-covid 10.5% loans on Mintos continue to be extended beyond limits, they just listed the same loans (30-day ES) at 17% yield. I cannot tell if they are super good at playing with Finance (including using the lamest possible Auditor for their non-publicly disclosed reports, as Mors highlighted) or they are struggling at finding cash. I completed my Creditstar portfolio move from Mintos to Lendermarket. I've now zero Creditstar on Mintos. I have the exact same exposure as before, but higher yield (from 10.5% to 14%) and better platform quality. The latter statement due to Lendermarket enforcing the 180D limit, while Mintos doesn't, and having no Pending Payment. I increased my IuteCredit bond position, since I found the current price a good deal. I've put them for sell at 100% so the next time there's a jump to 100% I could cash out my gain instantly. It's also more tax-efficient to get money from sales than from coupons in most Euro countries. Talking about bonds at par, 4Finance, who just re-installed their previous CEO, had their bond almost at par (99.65) the week before. My P2P portfolio somehow converged to the one of P2PMillionaire: thousands stuck in Varks recovery, some good quality low yield loans still in Mintos, plus Lendermarket. As him I bought the Varks with a nice discount, but in case of default, no matter the discount, you end at -100%  |

|

|

|

Post by geldregiertdiewelt on Oct 8, 2020 6:16:45 GMT

|

|

Money took 5 days to get transfered due to AML checks. As P2PMillionaire I invest through a legal entity for tax efficiency, but accounting is a bit more complicated.

Money took 5 days to get transfered due to AML checks. As P2PMillionaire I invest through a legal entity for tax efficiency, but accounting is a bit more complicated.