ashtondav

Member of DD Central

Posts: 1,805

Likes: 1,087

|

Post by ashtondav on Mar 14, 2016 13:47:14 GMT

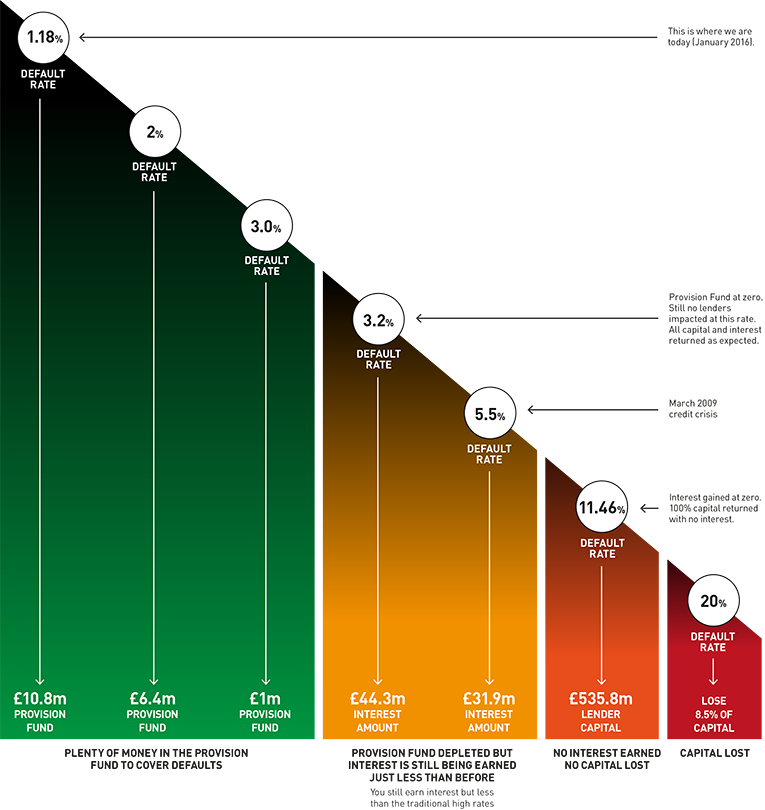

AFAIK only ZOPA was around in 2008. I recall that bad debt was a tidal wave that year. Assuming 2008 is "as bad as it gets" (yep it could be worse) would the RS & SG provision funds been adequate protection at that default level?

|

|

|

|

Post by chris on Mar 14, 2016 14:12:08 GMT

|

|

|

|

Post by westonkevRS on Mar 14, 2016 18:21:16 GMT

If your that way inclined, you can download BoE reported bad debt figures by quarter. Although it's hard to get a correlation because the numbers are only segmented by secured (meaning mortgages), student loans and other unsecured. This " other" category is only so useful because it includes high risk sub prime lending and credit cards, alongside your bog standard high-street loans and prime lending. However this segment " peaked" at an annualised bad rate of around 6.8% in a single quarter of 2009 (I'll check this percentage, as it's from memory. The chart 5.5% data was from some Equifax "run books" for fixed term loans, which seemed more comparable). That said, this was a peak and slowly improved therein. The chart above is based on a continuous annualised bad debt performance. Also every recession could be deeper, it's hard to know if it would be worse and what segments of society would be most affected. It's all guesswork. I've predicted personally 9 of the last 3 recessions....  Kevin. |

|

|

|

Post by chris on Mar 14, 2016 18:30:02 GMT

westonkevRS - as a student of the industry (techie learning finance through osmosis) I hope you don't mind me questioning you a little on this. I like to understand where other platforms are coming from as it is both a great way to learn and can be an inspiration for my own thinking. If you're not happy then let me know and I'll delete the post. Am I right in saying that should the loan book as a whole ever goes into the yellow zone on your chart that a resolution event is called? Is that something RS would have to do or is it something RS can choose to do? If an event is called what happens afterwards for the platform, would you effectively run down that loan book as a whole whilst starting up a new one? From what I've read thus far the next recession is unlikely to be the same as the last so it's very difficult to predict exactly how it will pan out. I'd just be interested in understanding what you're doing to mitigate against it, at least as much as you're willing to publicly declare to a competitor!

|

|

|

|

Post by westonkevRS on Mar 14, 2016 22:22:31 GMT

Specifics on when a resolution event would be called are not precise, and the specific actions taken not documented. This needs to be flexible as the events and economic scenario that would cause a resolution unknown. The Provision Fund web page states: www.ratesetter.com/lend/provisionfund" In the event of the Provision Fund becoming depleted, RateSetter would declare a ‘Resolution Event’. This would mean that all outstanding loan contracts would be automatically assigned to the Provision Fund, and all loan repayments would be collected by the Provision Fund on behalf of our investors.

Repayments would then be shared out (pro rata) to investors to ensure diversification of default risk. There would be a material delay in repayments being made." This would therefore probably be if we entered the yellow zone, and would probably means portfolio wind-down. But not necessarily, Zopa for example operated through the recession and returned lower (and in some cases reduced capital) interest. But they survived, rebuilt lender trust and today are considered robust and one of the safest P2P platforms. The other fact is that we have significant reporting and forecasting tools at our disposal. We can always treat future borrowers differently to avoid a resolution, but this is not ideal. RateSetter could also use it's own balance sheet, which is very strong, to capitalize the Provision Fund. There are many options and in reality RateSetter would do everything in its power to avoid a resolution, as it probably would be terminal to the brand. Kevin. |

|

|

|

Post by propman on Mar 15, 2016 8:25:37 GMT

Apologies for repeating what I have said elsewhere, but I think that calling a resolution event merely because some lenders are likely to receive a lower return than they expected (ie failure of "every penny on time") increases RS Platform risk. Zopa survived 2008 because it had never made any promise on default levels. Yes lenders were shocked and some left the market, but the vast majority continued to make better returns than they could get from a bank. Those that sat out the crisis did well as rates rose as a result of reduced fund availability and tightened credit, the investment Nirvana of lower risk and higher return.

IIRC the Zopa SG Fund reserves the right to reduce payouts if the fund is expected to be insufficient and so would continue to protect against catastrophic losses during a recovery period. I think continuing to pay capital when due would be seen as a good result from investors faced by a severe recession. It might take some rapid coding, but catch-up payments could be made when the level of net interest became clearer. Alternatively a "New" PF could be set up to give confidence to continuing investors that they weren't subsidising the previous bad debts, while ensuring that the old loans were repaid all that they had accrued in the fund. If The diversification of the full resolution event in the face of a severe downturn is thought necessary, then this should, in my opinion, be only if there is a significant risk of a loss of capital.

I would be interested to know what others think as I am convinced that RS as a whole will otherwise cease to continue in full in the next 30 years with the plan previously discussed of a full resolution event if any interest loss seemed inevitable (although the wording above seems to have been made more vague to perhaps allow what I propose). Of course part might be restarted, but the loss of volume would mean either most lenders would have had to leave, or rates would fall to levels unacceptable to most forum members (perhaps as a prelude to the loss of lenders required for a recovery).

|

|

pip

Posts: 542

Likes: 725

|

Post by pip on Mar 15, 2016 9:40:43 GMT

I think this graph is misleading for the following reason: - It quotes the default rate at the start of 2016 as 1.18%, while this is strictly true it's not the number that shows whether there is enough money in the provision funds to cover defaults as stated in the text below. The 1.18% is the defaults TO DATE (as at 1st January), what shows if there is enough money to cover defaults is anticipated bad debt over the course of the loans, which will be a lot higher.

|

|

|

|

Post by cassiopeia on Mar 23, 2016 8:47:10 GMT

How would the provision fund be used between small or large investors. Is it in proportion to the amount invested, so if in the event of a serious crisis everyone ends up the same % loss? Or is there any priority for small or long term investors?

|

|

toffeeboy

Member of DD Central

Posts: 506

Likes: 362

|

Post by toffeeboy on Mar 23, 2016 10:35:55 GMT

How would the provision fund be used between small or large investors. Is it in proportion to the amount invested, so if in the event of a serious crisis everyone ends up the same % loss? Or is there any priority for small or long term investors? In the event of a "resolution event" then no one would be given priority all outstanding loans would go into one pot and the money received shared out pro rata. Everyone would receive the same % loss, it wouldn't encourage new lenders if the old/larger lenders were to be looked after first.

This is only in the case of a "resolution event" which we all hope will never happen

|

|

spiral

Member of DD Central

Posts: 909

Likes: 456

|

Post by spiral on Mar 25, 2016 9:24:25 GMT

westonkevRSNice to see you have nothing better to do on an Easter weekend than hang around here.  Hopefully this will be quick and easy for you to answer.  The website says the PF is 17.6m with ~2.3% expected defaults and a coverage of 133% I equate this back to meaning you have about 575m in loans (couldn't see this on the website explicitly so feel free to correct me if I'm wrong) It also mentions 118m of secured loans with 152m security held. My question is, are these secured loans separate from the above or is the 118m part of the 575m? If it is part of the above figure (and I assume it is), how do you account for the security as part of the PF? Thanks

|

|

adrianc

Member of DD Central

Posts: 9,014

Likes: 4,825

|

Post by adrianc on Mar 25, 2016 9:32:58 GMT

|

|

spiral

Member of DD Central

Posts: 909

Likes: 456

|

Post by spiral on Mar 25, 2016 11:39:08 GMT

I wasn't logged in so that's probably why I wasn't seeing it. Anyway, nice to see the sums add up.  |

|

|

|

Post by westonkevRS on Mar 25, 2016 19:28:28 GMT

westonkevRS Nice to see you have nothing better to do on an Easter weekend than hang around here. Hopefully this will be quick and easy for you to answer. The website says the PF is 17.6m with ~2.3% expected defaults and a coverage of 133% I equate this back to meaning you have about 575m in loans (couldn't see this on the website explicitly so feel free to correct me if I'm wrong) It also mentions 118m of secured loans with 152m security held. My question is, are these secured loans separate from the above or is the 118m part of the 575m? If it is part of the above figure (and I assume it is), how do you account for the security as part of the PF? Thanks The £575m is the total outstanding balances, so the secured loans are part of this. In theory they are expected to have less need of the Provision Fund, but if all things failed the Provision Fund is liable. A small note, many lenders quite rightly compare the size of the Provision Fund to this £575m balance. This is logical but unfortunately isn't accurate, because within the £575m are loans funded by "institutions" that don't have access to the fund, i.e. a default would mean this specific lender type wouldn't be paid back and the Provision Fund would not be depleted. Additionally the £575m includes loans that if they default are paid by a business partner rather than the Provision Fund. All this means is that actually the Provision Fund is covering a number far less than £575m, but currently for commercial confidentiality we cannot publish this differential. We are working on this though, because we know it makes the fund look weaker than it actually is. Kevin.

|

|

jimc99

Member of DD Central

Posts: 284

Likes: 115

|

Post by jimc99 on Mar 25, 2016 21:32:07 GMT

Well I have been running down my RS investments just because the Provision Fund appears to be getting weaker and weaker. So I'd really like to know the true cover (% of outstanding loans) it provides for me....just a normal investor. Not a director or institution or any other non individual body RS loans out money for!!

Why bother showing the Provision Fund details when they are apparently so misleading...and in a negative way to boot!!!

|

|

|

|

Post by westonkevRS on Mar 26, 2016 9:40:06 GMT

I know, it is a little frustrating and something we are going to address. It's the same with the coverage ratio where we are super prudent, e.g. ignoring future contributions from default recoveries, payment plans and lifetime contributions. As a result you are not alone, lenders think we are riskier than we are and either leave or recommend others sites as safer. It's not their fault, they are unfortunately ignorant of all the facts and so cannot make an informed decision.

Those organizations that have all the facts have correctly determined us as the safest site, Which! and 4th Way as two examples. But reviews by a credit reference agency and an institution have come to similar (confidential) conclusions.

But we think this will be proven in the long run. RateSetter will let it's long term performance do the talking, actions not words. For example the Provision Fund now has £17.6m, and although 2015 wasn't as credit good as 2012-2014, I'm bullish for 2016!

Kevin.

|

|