bigfoot12

Member of DD Central

Posts: 1,817

Likes: 816

|

Post by bigfoot12 on Mar 29, 2018 15:00:11 GMT

I could see that it might be possible to have some sort of proof of ownership that is published and yet secret. This might be useful in an insolvency, and so inspire confidence, but this would still need some sort of secret yet independent audit from an accountant or regulator if it were to help reduce the risk of fraud. But most of your other claims I struggle to see what use it might be:- Sorry which transaction fees will block chain reduce and how? I can't see it reducing the fees for me paying into my account in GBP, nor similarly paying out for the borrower. Any internal movement within the platform has no cost now so I am confused. The only significant implementation of blockchain has transaction fees orders of magnitude larger than those most us of pay. secondary market improvements (buy/sell orders) How will blockchain improve these? These are all done through the platform, no need for some sort of distributed database, a central one is fine. cross border lending via smart contracts etc. Again I don't understand, how blockchain would help. People lend like this now without blockchain. And the risks now are currency moves, and not understanding the process and trustworthyness in other countries. (I am not saying people are less trustworthy in other countries, just that it might be easier to recognise them in our own country.) Block chain doesn't change this. Personally I am nervous about lending in Scotland and Northern Ireland because I don't understand how the insolvency process works there (and I'm not sure some platforms do either). And no smart contract is going to fix these issues. |

|

cb25

Posts: 3,523

Likes: 2,666

|

Post by cb25 on Mar 29, 2018 16:46:47 GMT

Like bigfoot12 I can't see the advantage of blockchain here, at least for the first two items mentioned: 1. Fees. Imo technology costs, along with labour costs, might set a minimum for the fees charged by a platform, but the real determinant is what the platform thinks the market will accept. E.g. FC have been charging lenders 1% since FC were small (where they no doubt needed that level), but still charge it now (when you think economies of scale would have allowed it to be reduced). FC almost certainly could reduce fees and still make a profit, but there's no market pressure to do so, so they don't. 2. Secondary markets. Key factor here seems (to me) to be platform design, not technology constraints. With FC in the old days, if you saw (say) a £20 loan on the SM you could buy it instantly. Compare that to AC now, you see a loan with £1000s available, put it a buy order, but it's not fulfilled instantly as AC appear to batch up the requests (why ??). I'm sure it's not down to AC having less capable technology than FC of old, simply that AC have designed their SM in that rather (silly) way. Regardless of whether I'm looking at P2P, banking, shares etc. I concentrate on whether it's regulated, secure, easy to use, fast enough, acceptable fees. I don't care what technology is used to achieve it, only what it delivers. |

|

gibmike

Member of DD Central

What is a cynic? A man who knows the price of everything and the value of nothing.

Posts: 255

Likes: 159

|

Post by gibmike on Mar 29, 2018 20:32:35 GMT

Like bigfoot12 I can't see the advantage of blockchain here, at least for the first two items mentioned: 1. Fees. Imo technology costs, along with labour costs, might set a minimum for the fees charged by a platform, but the real determinant is what the platform thinks the market will accept. E.g. FC have been charging lenders 1% since FC were small (where they no doubt needed that level), but still charge it now (when you think economies of scale would have allowed it to be reduced). FC almost certainly could reduce fees and still make a profit, but there's no market pressure to do so, so they don't. 2. Secondary markets. Key factor here seems (to me) to be platform design, not technology constraints. With FC in the old days, if you saw (say) a £20 loan on the SM you could buy it instantly. Compare that to AC now, you see a loan with £1000s available, put it a buy order, but it's not fulfilled instantly as AC appear to batch up the requests (why ??). I'm sure it's not down to AC having less capable technology than FC of old, simply that AC have designed their SM in that rather (silly) way. Regardless of whether I'm looking at P2P, banking, shares etc. I concentrate on whether it's regulated, secure, easy to use, fast enough, acceptable fees. I don't care what technology is used to achieve it, only what it delivers. 1. Transaction fees, speed of funds, vetting of lenders, kyc there are a lot of overheads. 2. Swapping tokens between parties will be quicker and smarter. 3. Smart contracts are a big factor. Over time investors and borrowers will benefit hugely from cost benefits both in terms of improved returns and time. Imagine a cross platform exchange allowing you to trade tokens across AC/ FC/ ABL etc. who are all regulated and working to a set of guidelines. This creates a great barrier to entry for these guys AND it provides some security for us in knowing they are regulated.

|

|

p2pete

Member of DD Central

Posts: 144

Likes: 142

|

Post by p2pete on Mar 29, 2018 21:59:15 GMT

Compare that to AC now, you see a loan with £1000s available, put it a buy order, but it's not fulfilled instantly as AC appear to batch up the requests (why ??). I'm sure it's not down to AC having less capable technology than FC of old, simply that AC have designed their SM in that rather (silly) way. Yes it's awful, and to make matters worse they label it as 'available for instant investment'. Then you sit in a non-existant queue for 3 days. It's really bad design and coding. It's infuriating as a lender, imagine how the borrowers would feel if they knew lenders were trying to lend but the platform won't let them.

|

|

|

|

Post by Deleted on Mar 30, 2018 16:50:33 GMT

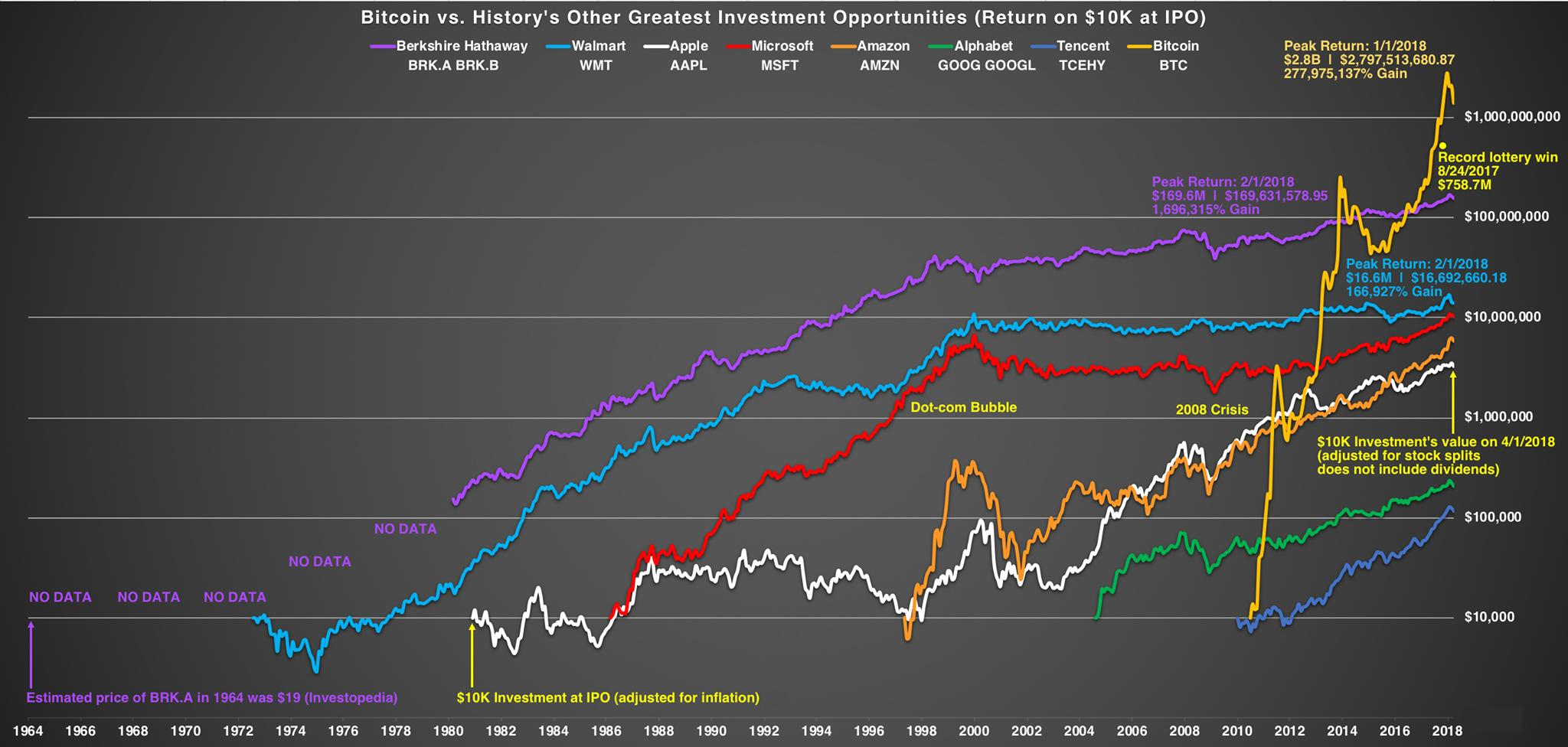

With Bitcoin at it's lowest point since it's meteoric rise late last year is anyone else tempted to top up their holdings in Crypto?

I've thought for a while if it drops below $7k I'd increase Crypto to 3% of net worth. At least that way if it all goes to nothing it's less than a yrs interest elsewhere!

|

|

Liz

Member of DD Central

Posts: 2,426

Likes: 1,297

|

Post by Liz on Apr 1, 2018 10:31:55 GMT

With Bitcoin at it's lowest point since it's meteoric rise late last year is anyone else tempted to top up their holdings in Crypto? I've thought for a while if it drops below $7k I'd increase Crypto to 3% of net worth. At least that way if it all goes to nothing it's less than a yrs interest elsewhere! No, the fall shows no sign of stopping anytime soon.

|

|

SteveT

Member of DD Central

Posts: 6,873

Likes: 7,918

|

Post by SteveT on Apr 1, 2018 10:37:31 GMT

No, the fall shows no sign of stopping anytime soon. Indeed. On the plus side, the premium over Bitcoin's intrinsic NAV is now down to barely $6600. Bargain

|

|

Liz

Member of DD Central

Posts: 2,426

Likes: 1,297

|

Post by Liz on Apr 1, 2018 10:56:51 GMT

No, the fall shows no sign of stopping anytime soon. Indeed. On the plus side, the premium over Bitcoin's intrinsic NAV is now down to barely $6600. Bargain If you had bought Ether for example after its Feb fall from near 1400 to 800, you would have been up 20% In a few days, but today you would be down over 50%. Bitcoin is holding up better than most and is an increasing percentage of the overall crypto market.

|

|

|

|

Post by Deleted on Apr 1, 2018 13:43:19 GMT

No, the fall shows no sign of stopping anytime soon. Indeed. On the plus side, the premium over Bitcoin's intrinsic NAV is now down to barely $6600. Bargain you must have tempted me as I took the plunge for a little more at $6500, you did say it was a bargain right ?? I've got the years ahead and appetite for a little gamble, 2-3% of portfolio (I have a little headroom yet for more if it bottoms significantly lower). If it all goes it goes, so be it, but if it booms again I'll sell down to cover my investment. Now ... perhaps I should consider winding down my Lendy holdings, I'm not sure I have the appetite for the double gamble

|

|

|

|

Post by charlata on Apr 10, 2018 19:00:28 GMT

I've often wondered how one might go about modelling the value of something with no dividend, no prospect of a dividend and no utility value. Turns out there's a simple solution. Bitcoin's price is determined by the ratio of infection/recovery for the bitcoin meme, so you use an epidemiological model. This begs the question of how many susceptible individuals remain to be drawn into bridging loans where the ROI is shared 50:50 with the platform. |

|

GeorgeT

Member of DD Central

Posts: 1,321

Likes: 1,575

|

Post by GeorgeT on Apr 14, 2018 20:14:19 GMT

I've got Bitcoin and Ethereum and I was a little bit down on my holding after the fall over the last month but I'm pleased to say that in the last few days cryptos are starting to recover very nicely.

However if I can get back into profit territory I am going to sell out on paxful.

|

|

|

|

Post by nellerdk on Apr 18, 2018 17:35:06 GMT

|

|

SteveT

Member of DD Central

Posts: 6,873

Likes: 7,918

|

Post by SteveT on Nov 19, 2018 17:21:49 GMT

Indeed. On the plus side, the premium over Bitcoin's intrinsic NAV is now down to barely $6600. Bargain you must have tempted me as I took the plunge for a little more at $6500, you did say it was a bargain right ?? I've got the years ahead and appetite for a little gamble, 2-3% of portfolio (I have a little headroom yet for more if it bottoms significantly lower). If it all goes it goes, so be it, but if it booms again I'll sell down to cover my investment. Now ... perhaps I should consider winding down my Lendy holdings, I'm not sure I have the appetite for the double gamble I hope you bailed out a while back. Down to around $5000 today. Good news is that the downside risk is now much reduced (to approx $5000)

|

|

|

|

Post by Deleted on Nov 19, 2018 19:10:25 GMT

SteveT you must have tempted me as I took the plunge for a little more at $6500, you did say it was a bargain right ?? I've got the years ahead and appetite for a little gamble, 2-3% of portfolio (I have a little headroom yet for more if it bottoms significantly lower). If it all goes it goes, so be it, but if it booms again I'll sell down to cover my investment. Now ... perhaps I should consider winding down my Lendy holdings, I'm not sure I have the appetite for the double gamble I hope you bailed out a while back. Down to around $5000 today. Good news is that the downside risk is now much reduced (to approx $5000) Impressive you thought of me as the bad news hit new landmarks, I unfortunately continue to hold bitcoin as part of a wider Crypto portfolio on ICONOMI. I'll freely admit it's lost close to half it's value but it was always a gamble and I clearly bought too much at the height of the hype. However it was always a small portion of my overall so given the downside is now significantly reduced I'll continue to hold because, well why not .... I won't overly miss it if it all goes and who knows what upside a long term hold might bring.

|

|

bigfoot12

Member of DD Central

Posts: 1,817

Likes: 816

|

Post by bigfoot12 on Nov 23, 2018 18:33:28 GMT

From the BBC website "Barclaycard said it had processed 1,087 transactions per second between 13:00 and 14:00 GMT"! Chew on that Bitcoin! |

|